Market overview: A 25bp hike, but the message matters more

The ECB looks firmly on course to raise rates by 25bp on 11 June. Policymakers have guided markets towards that outcome with little room for surprise, and a hold would risk unsettling credibility at a time when the central bank is still trying to avoid any echo of the 2022 inflation shock.

A larger 50bp move cannot be fully ruled out in theory, but it looks unnecessary. Markets already price further tightening later this year, so the ECB does not need to shock investors to reinforce its anti-inflation stance.

The real test is the tone. A 25bp hike is fully discounted, which shifts attention to the press conference and the ECB’s forward-looking language. With around 64bp of total tightening priced by year-end, President Christine Lagarde and the Governing Council are likely to focus on keeping those expectations intact.

This is less about conviction and more about insurance. Energy prices, geopolitical risk and second-round inflation effects remain difficult to judge, making staff forecasts less reliable than usual. In that context, inflation expectations become the key battlefield. The ECB’s safest option is to sound hawkish now, preserve optionality and wait for clearer signals from the data.

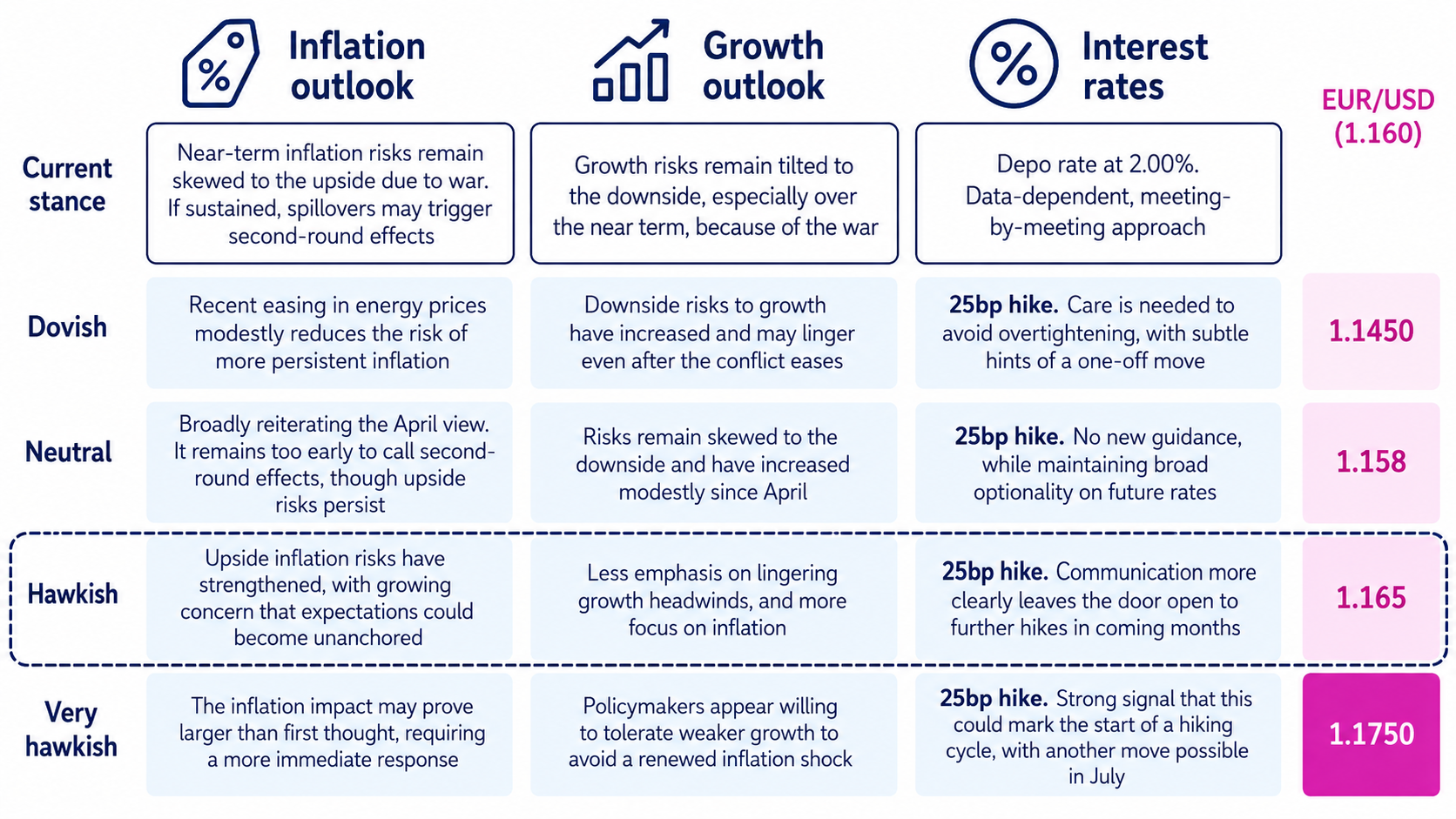

Our base case is therefore a hawkish 25bp hike. We do not think the ECB needs to pre-commit to further moves in July, September or the fourth quarter, although the risk of a follow-up increase later in the year has clearly risen. For now, we still see June as a one-and-done move.

Rates: The ECB needs to avoid sounding too relaxed

Markets have already absorbed the June hike, but confirmation could still apply modest upward pressure across the curve. Any guidance that leaves the door open to further tightening should keep front-end rates supported, while a stronger focus on inflation risks may also lift inflation pricing.

A dovish surprise would be risky. If the ECB leans too heavily into a one-and-done message, markets could lower near-term tightening expectations, pulling 2-year rates down. But longer-dated yields may prove stickier if investors conclude that a softer ECB stance raises future inflation risk. The result would likely be a steeper curve.

That makes a hawkish communication strategy the cleaner choice. Current pricing already assumes another move by September, and pushing too hard against that view could loosen financial conditions at the wrong moment.

Growth risks still matter, however. Sentiment has been resilient, helped by strong US equities, but the balance is not robust. If the ECB places greater weight on downside growth risks, rates could face broader downward pressure.

EUR/USD: Hawkish ECB tone can keep the euro supported

Short-term rate spreads have become a more important driver of EUR/USD again. A hawkish repricing of the Fed, alongside doubts over the ECB tightening path, has widened the EUR 2-year swap differential by around 25bp since the end of April.

That move is a headwind for EUR/USD, all else equal. Even so, the pair can still hold above 1.160 as long as oil prices remain contained. A hawkish ECB hike on 11 June should help defend that equilibrium and provide a stronger base for the euro if geopolitical risks ease.

Our baseline points to upside risk for EUR/USD on the day, with the near-term bias still constructive. We remain modestly bullish into the summer and look for a gradual move back towards 1.180 in a de-escalation scenario.

Mapping Lagarde’s possible paths

Looking ahead

- The ECB is expected to deliver a 25bp hike on 11 June.

- The market reaction will depend more on guidance than the rate decision itself.

- A hawkish tone should help keep inflation expectations anchored.

- Rates are likely to be more vulnerable to dovish language than to the hike itself.

- EUR/USD should remain supported if the ECB preserves tightening optionality and energy prices stay contained.

- A move towards 1.180 remains plausible if geopolitical risks fade.