03 June 2026

News

FX markets stay calm as yield demand returns

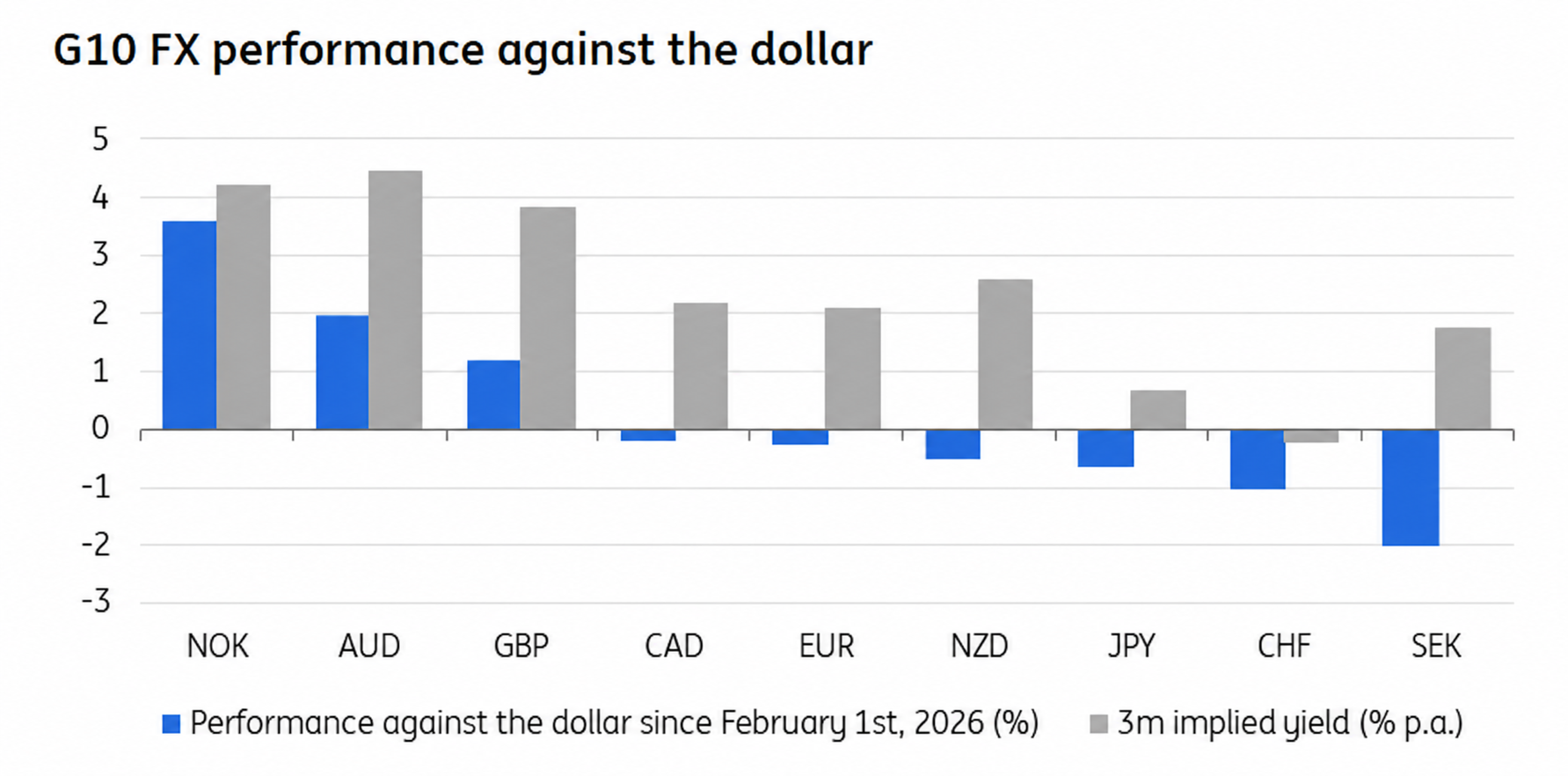

Across asset classes, FX markets have adopted a broadly constructive, “glass half full” tone, much like equities and credit. After a brief spike in March, traded FX volatility has fallen back toward the lower end of its three-year range. As is often the case, lower volatility has encouraged investors to seek yield, with higher-yielding currencies in demand across both developed and emerging markets.

High-yielding currencies remain well supported

Within developed markets, this has supported outperformance in both the Norwegian krone and the Australian dollar. Both currencies offer implied yields above 4% and have positive exposure to the energy theme. In addition, both Norway and Australia have seen a marked improvement in their terms of trade over the past eight weeks. Their central banks have also raised rates during the crisis and continue to leave the door open to further tightening. We expect these currencies to remain well supported.

Low yielders remain under pressure

At the other end of the spectrum are low-yielding currencies, particularly those vulnerable to higher energy import costs. The yen stands out in this regard, especially as the Bank of Japan has been slow to raise rates, leaving real interest rates deeply negative. So far, it appears the BoJ has spent roughly $70bn defending the key 160 level in USD/JPY. However, intervention looks less fundamentally justified than it did in 2024, when the Fed was preparing to ease policy. We suspect this marks the beginning of a prolonged battle between the BoJ and the market around the 160 level.

Dollar outlook remains mixed

Somewhat surprisingly, the dollar has ranked in the middle of the G10 FX pack over the past eight weeks. In theory, it should have performed better, given US energy independence and a difficult backdrop for risk assets. One factor holding the dollar back has likely been the global equity rally, as the correlation between equity gains and dollar weakness has strengthened. This is particularly evident in emerging markets, where investors have maintained the long positions built up between last summer and February this year.

We remain bearish on the dollar over a multi-quarter horizon, as the Fed should eventually have room to cut rates back toward neutral. We also note that very little risk premium is currently priced into the dollar, something that could change ahead of the US mid-term elections in November. That said, developments in Iran will play an important role in determining the timing of any dollar sell-off. The longer energy prices remain elevated, the greater the chance that the Fed will need to maintain a hawkish tone to manage the inflation shock. This could support the dollar while weighing on risk assets.

EUR/USD may remain range-bound for now

For EUR/USD, this points to further trading within the 1.16–1.18 range through the second quarter. However, the ECB will need to raise rates in June and maintain a hawkish message to keep real interest rates elevated during this period of high inflation. Later in the year, EUR/USD levels above 1.20 remain entirely plausible, provided the global economy stabilises and the broader investment theme of diversifying away from US risk resumes.