Executive summary

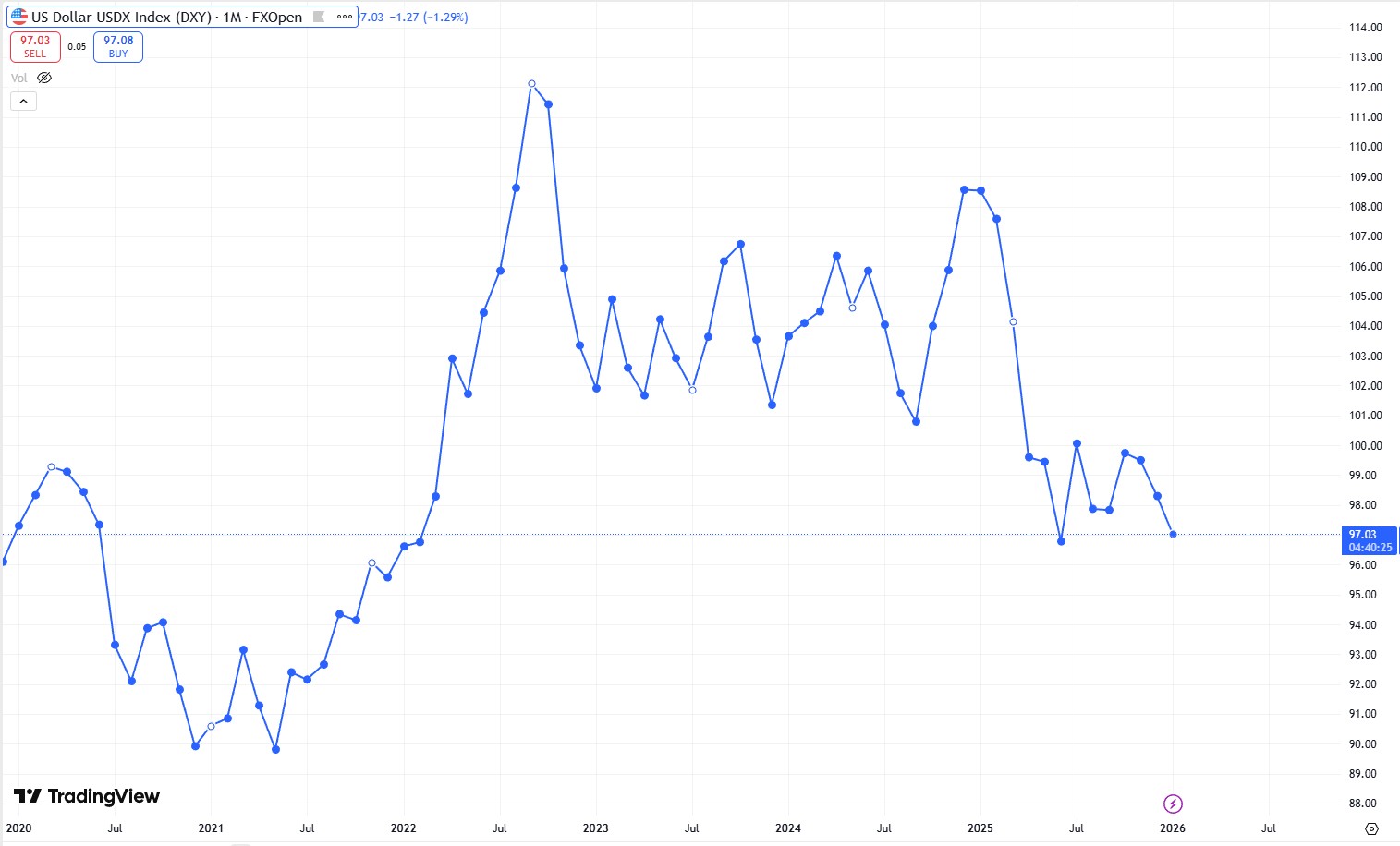

The US dollar (USD) has long been viewed as the world’s primary safe-haven currency. However, it has depreciated by around 14% from its September 2022 peak, and recent US policy developments have raised fresh doubts about whether the dollar can sustain the same level of trust. This report reviews the drivers behind the dollar’s weakness, assesses the durability of its safe-haven role, and outlines plausible short-, medium-, and long-term scenarios for USD performance.

Key takeaways

-

Safe-haven status under scrutiny: The dollar’s sharp decline was amplified by unpredictable tariff actions and rising fiscal concerns, which weakened confidence in the USD’s traditional safe-haven role.

-

Further weakness remains possible: A reduced appeal of US assets, particularly if the interest-rate advantage continues to erode, points to additional USD depreciation over the medium term.

-

Policy risks are central: Deliberate debasement appears unlikely, but erratic policymaking and perceived threats to institutional credibility could continue to undermine confidence in the currency.

Short term: What drove the recent decline in the US dollar?

In the run-up to the US election on 5 November 2024, and immediately after it, the USD strengthened as markets priced in the prospect of continued US asset outperformance. Investors expected a pro-growth agenda led by deregulation, government efficiency initiatives, and additional corporate tax cuts.

That optimism began to fade as trade policy became more confrontational. The turning point came on the administration’s so-called Liberation Day on 2 April, when punitive reciprocal tariffs were announced. The surprise triggered a sharp sell-off, with the USD weakening by more than 10%.

Negative sentiment deepened as investors began questioning the dollar’s safe-haven characteristics, particularly when the currency appeared to decouple from the usual support of higher US interest rates following the tariff shock. Further pressure came from the passage of the One Big Beautiful Bill Act, reinforcing expectations of persistent budget deficits and a challenging debt trajectory, as well as ongoing public pressure on the Federal Reserve to lower interest rates, raising concerns about policy credibility and the stability of the monetary framework.

At the same time, cyclical concerns contributed to weakness. Markets worried that protectionist policies could increase the risk of US stagflation. As new trade deals emerged and worst-case tariff outcomes did not materialise, confidence partially recovered. From summer 2025, the USD largely traded sideways, supported in part by strong investment inflows linked to exceptional performance in the artificial intelligence sector.

Assessing the safe-haven question: Why did the USD fail to rally during volatility?

In early 2025, the USD did not consistently appreciate during periods of market stress, raising doubts about its safe-haven behaviour. Historically, however, the USD tends to perform best as a safe haven when global growth is slowing or the world is moving toward a broad-based recession. The dollar does not always strengthen when uncertainty originates in the US itself.

A useful historical parallel is the 2008 financial crisis. Early in the episode, the USD weakened as the crisis began in the US, then strengthened as stress became global and demand rose for dollar liquidity and US Treasury assets. In that context, the USD’s weakness following the Liberation Day tariff shock is less surprising, because the initial policy risk was perceived as disproportionately harmful to the US economy.

What would it take for the USD to lose safe-haven status?

A lasting loss of safe-haven status would likely require policies that meaningfully weaken the foundations of US stability and investor trust. In practical terms, that would mean sustained deterioration in institutional strength and predictability, the rule of law and property-rights confidence, and monetary-policy independence and credibility.

A policymaking style that relies heavily on executive action while bypassing established institutional checks can elevate perceived system risk. If investors conclude that institutional credibility is weakening, the reputational premium that supports US assets and, by extension, the USD could diminish further.

Medium term: Why further weakness remains plausible

While the USD’s decline has reduced some of its prior overvaluation, the currency still appears to have room to fall. Three drivers are particularly relevant.

Structural outflows linked to the twin deficit

The US twin deficit, meaning the combination of budget and trade deficits, increases USD vulnerability because the system relies on steady foreign capital inflows to offset net outflows. If inflows slow, downward pressure on the currency increases. US asset attractiveness has been supported by the AI-led boom, but that support could fade if US rate cuts narrow the still-favourable interest-rate differential, or if markets begin questioning the durability of superior US returns.

Fiscal risks that could re-enter focus

Although markets debated the One Big Beautiful Bill Act before it passed, investor attention moved on quickly afterwards. Even so, the legislation reinforces expectations of high deficits for years. If tariff revenues do not meaningfully narrow the fiscal gap, fiscal sustainability concerns could return. If US Treasuries become less attractive to hold, weaker foreign demand would likely translate into reduced inflows and renewed USD weakness.

Persistent risk of policy volatility

Trade tensions have eased at times, and policymaking could become more growth-supportive ahead of the 2026 midterm elections, but the risk of renewed volatility remains. Continued pressure on the Federal Reserve to cut rates keeps investor attention on the perceived independence of monetary policy. Any material increase in distrust toward US assets, particularly Treasuries, could lead to fewer inflows, a weaker dollar, and further questions over safe-haven status.

Key risk: Is the US trying to engineer a weaker dollar?

A politically motivated preference for a weaker USD has been widely discussed since President Trump’s inauguration, including speculation about a so-called Mar-a-Lago agreement similar to the 1985 Plaza Accord. That debate has cooled. Beyond pressure for lower rates, there have not been clear, sustained policy moves explicitly designed to depreciate the currency.

Importantly, deliberate depreciation would conflict with the advantages the US derives from the dollar’s reserve-currency role, including lower financing costs and geopolitical leverage. As a result, the USD’s 2025 weakening appears more consistent with an unintended, or at least tolerated, side effect of erratic policymaking than with a coordinated strategy of depreciation or debasement.

Long term: A constructive scenario for the US dollar

A positive risk scenario remains plausible. If policy volatility declines ahead of the 2026 midterms, or if the administration pivots to reduce economic damage from tariffs, confidence in US assets could improve. That would support sustained capital inflows and allow the USD to regain ground.

The US is still expected to grow faster and offer higher interest rates than many peer economies in 2026. If markets refocus from institutional credibility concerns toward traditional drivers such as growth and interest-rate differentials, the USD’s outlook would improve. This would resemble the pattern seen during the first Trump presidency, when the USD weakened early in the term as trade conflict intensified, then stabilised and recovered as policy emphasis shifted toward more growth-supportive measures approaching midterm elections.

Frequently asked questions

Why has the USD weakened since 2022?

The USD peaked as markets anticipated a turning point toward Federal Reserve rate cuts. It then depreciated more sharply in early 2025 as trade-policy volatility and fiscal concerns undermined confidence in US assets and the dollar’s safe-haven appeal.

Is the USD losing its safe-haven character?

Its safe-haven status is being tested, not eliminated. The USD typically behaves as a safe haven most reliably during global recessions or widespread stress, rather than when uncertainty is primarily US-driven.

Could political decisions weaken the USD further?

Yes. Policies that increase uncertainty, impair institutional credibility, or raise doubts about monetary-policy independence could further erode trust and contribute to additional depreciation.

Is deliberate depreciation likely?

It appears unlikely, given the strategic and financial benefits the US derives from the dollar’s reserve-currency role. However, some policy choices may still result in a weaker USD as a secondary effect.

What could strengthen the USD again?

A sustained reduction in policy volatility, coupled with growth-friendly measures ahead of the 2026 midterm elections, could restore investor confidence and maintain inflows into US assets, supporting a firmer USD.