05 June 2026

In focus

- Monfor Dealing Team

- News

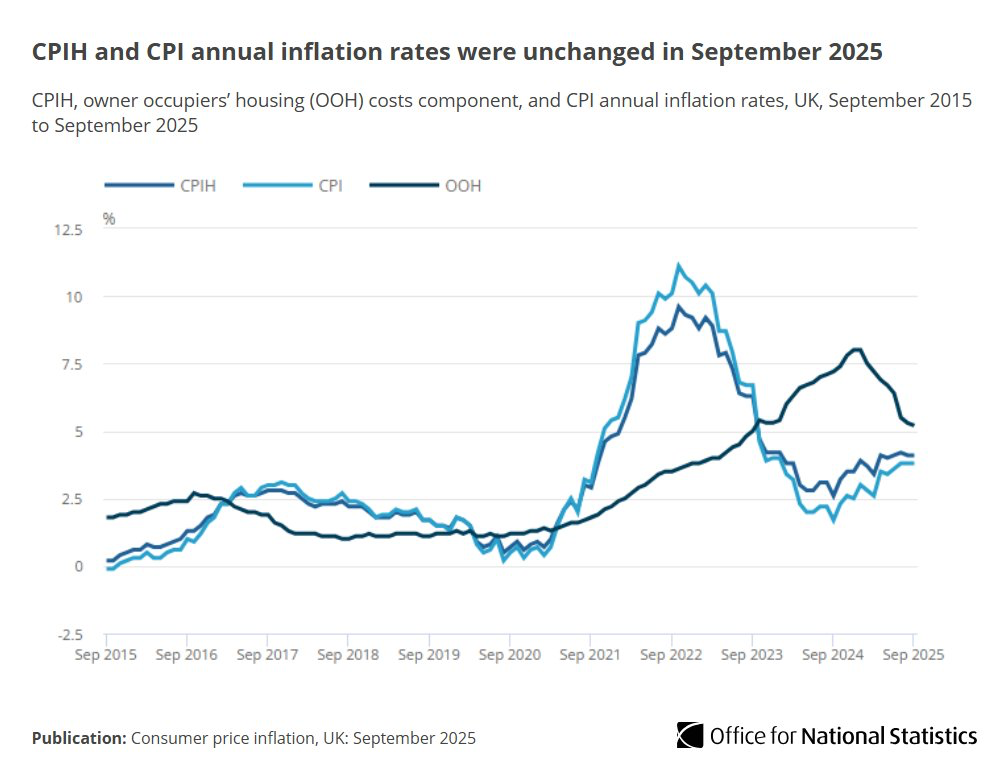

Pound slips as UK inflation undershoots expectations

- Monfor Dealing Team

- News

GBP: Softer inflation data weighs on the pound

UK inflation figures released this morning came in softer than expected across both headline and core readings. Core CPI, which excludes food and energy prices, eased to 3.5% year-on-year, below the 3.7% forecast. Services inflation – closely monitored by the Bank of England for signs of persistent price pressure – held steady at 4.7%, just under expectations. Meanwhile, food inflation slowed for the first time since March, falling from 5.3% to 4.9%.

The weaker data prompted a swift reaction in sterling, which slipped by around 0.3% against the dollar and underperformed across the G10 space. With markets positioned for stickier inflation, the softer print caught many off guard and revived speculation that the Bank of England could deliver a rate cut in December.

Sterling’s recent recovery has faltered, with GBP/USD unable to push above the 21-day moving average, and the pair now trading almost 2% below its mid-September highs near 1.3726. The pound-to-euro rate has dropped back under 1.15, while the pound-to-dollar rate sits around 1.3350. Although the weaker inflation outcome offers some relief for households and businesses, the long-held rule still applies: softer inflation tends to weaken the currency.

EUR: Political uncertainty keeps the euro under pressure

The euro edged lower once again, slipping toward the 1.16 support level and extending its weekly decline to around 0.4% against the dollar. Pressure was particularly visible in EUR/CHF, which has fallen below the 0.93–0.94 range that held firm for most of the past year, now hovering just above 0.92.

The move reflects persistent unease around France’s political backdrop, where investor caution remains elevated despite Defence Minister Lecornu’s re-election and a solid run of French corporate earnings. These results helped French equities climb above their May 2024 record high, but they have done little to dispel concerns that political gridlock could hamper economic momentum.

French–German bond spreads continue to trade near 80 basis points, signalling that political risk premia remain entrenched. Until clearer signs of political stability emerge, the euro’s upside is likely to stay limited.

USD: Dollar gains on yen weakness and trade optimism

The dollar extended its advance yesterday, with the DXY index climbing 0.3% and edging closer to the 99.00 level. The move was driven primarily by a weaker yen following Sanae Takaichi’s victory in Japan’s parliamentary vote, which spurred selling pressure through both the London and New York sessions.

Sentiment was boosted further by remarks from President Trump, who voiced confidence in achieving a “really fair and really great” trade deal with President Xi ahead of their planned meeting in South Korea. He also reiterated his willingness to raise tariffs on Chinese goods if no agreement is reached by 1 November, signalling both optimism and firmness in his stance.

Gold and silver fell sharply, dropping 5.3% and 7.1% respectively in one of their steepest one-day declines in nearly five years. The retreat highlights reduced demand for safe havens as improving trade sentiment and a stronger dollar dampen their appeal. Despite a lack of fresh data, the dollar’s strength has surprised markets, appearing somewhat detached from the Federal Reserve’s recent dovish tone. Investors now await new economic indicators to determine whether the Fed’s softer outlook is justified.

Looking ahead: Inflation data in focus

The next key driver for markets will be Friday’s US inflation report, which could define short-term dollar direction. A stronger-than-expected result would likely push EUR/USD below the 1.16 level and reinforce the greenback’s recent momentum.

For sterling, near-term trading is likely to remain subdued as markets position for a possible Bank of England rate cut. Even so, the broader outlook remains unchanged: sustained signs of economic improvement should ultimately lend support to the pound over time.