08 June 2026

News

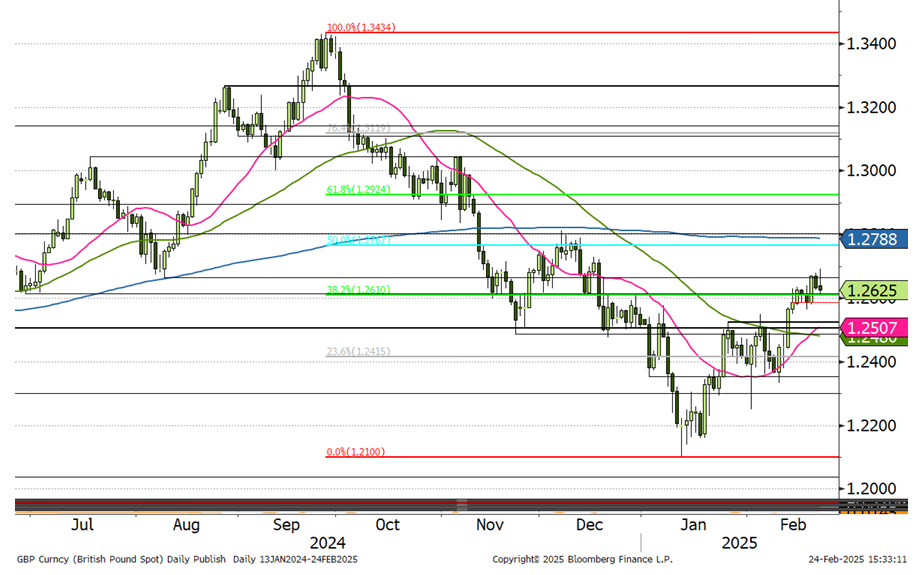

Sterling Highly Exposed to Potential Market Correction

The British pound remains at significant risk of a downturn should global markets shift towards a risk-off sentiment, according to a research note from BNP Paribas. The bank identifies Sterling as one of the most vulnerable currencies among its G10 peers, citing structural weaknesses and heightened sensitivity to investor risk appetite.

This warning comes amid prevailing risk-on market conditions, in line with the ongoing bull run in equities, which has supported recent gains in the pound’s exchange rate. The recent setback in the pound-to-euro exchange rate recovery aligns with a dip in the U.S. S&P 500 index, widely regarded as a benchmark for global investor sentiment.

While the decline has been relatively modest, it underscores Sterling’s sensitivity to broader market trends, suggesting that a more substantial market correction could trigger far greater losses. A key vulnerability is the UK’s deteriorating net international investment position (NIIP) and its persistent current account deficit, which has left the currency reliant on foreign capital inflows.

The research also highlights Sterling’s susceptibility to a broader economic slowdown, placing it alongside emerging market high-yield currencies such as the Brazilian real and the Hungarian forint. In contrast, safe-haven currencies such as the Japanese yen and Swiss franc are expected to outperform in risk-off conditions.

UK: Bank of England Speakers in Focus

In the UK, while no major economic data releases are scheduled, several members of the Bank of England’s Monetary Policy Committee (MPC) will be speaking throughout the week. Deputy Governor for Monetary Policy Clare Lombardelli will deliver the opening remarks at the annual BEAR conference on Monday, with Chief Economist Huw Pill set to provide the closing remarks—comments that are typically closely scrutinised by markets.

Later in the day, Dave Ramsden will discuss the Bank’s balance sheet ahead of a key decision on its future structure later this year. He is scheduled to speak again on Friday, providing ample opportunity to address interest rate policy. Ramsden is considered ‘dovish,’ and markets will be keen to determine whether he may vote for another interest rate cut next month.

Swati Dhingra is also due to speak and is widely expected to confirm her preference for another rate cut, though her stance is well known and unlikely to impact markets significantly. Following last week’s stronger-than-expected economic data, market expectations for Bank of England rate cuts this year have been pared back, with only two more reductions now priced in. The Bank itself has indicated a preference for around three further cuts, maintaining its quarterly pace.

As a result, some dovish MPC members may attempt to guide markets towards greater expectations of easing, which could put pressure on Sterling. However, any downside is likely to be limited, as economic fundamentals suggest inflation risks remain skewed to the upside, restricting the Bank’s scope for further cuts.

EUR/USD – Bulls Holding Firm

EUR/USD gained bullish momentum on Tuesday, closing in positive territory. While the pair remains relatively steady around 1.0500 in Wednesday’s European morning session, technical indicators suggest little sign of a deeper correction. Tuesday’s sharp decline in US Treasury bond yields weighed on the US dollar, helping EUR/USD push higher.

US Treasury Secretary Scott Bessent stated that President Donald Trump’s administration aims to reduce spending while simultaneously easing monetary policy and lowering Treasury yields. Following these comments, the benchmark 10-year US yield dropped more than 2% on the day, touching its lowest level since early December at below 4.3%.

President Trump is set to hold a press conference at 14:00 GMT, with investors closely watching for remarks on tariff policy. A further decline in US bond yields could put renewed pressure on the dollar, paving the way for additional gains in EUR/USD. As of the latest update, the 10-year yield had edged slightly higher to 4.305%.

The Relative Strength Index (RSI) on the four-hour chart remains above 50, and EUR/USD continues to trade above its 20-period and 50-period Simple Moving Averages (SMA), indicating a lack of strong selling pressure. EUR/USD faces key resistance at 1.0500-1.0510 (round level, Fibonacci 78.6% retracement of the recent downtrend), with further resistance at 1.0540 (100-day SMA) and 1.0600 (starting point of the previous downtrend).

On the downside, support levels are observed at 1.0440 (Fibonacci 61.8% retracement), 1.0390-1.0400 (50-day SMA, Fibonacci 50% retracement), and 1.0350 (Fibonacci 38.2% retracement).